Most organizations read defense policy documents for compliance. They scan for provisions that affect current contracts, flag new restrictions, and move on. That is the minimum viable use of a document that contains considerably more.

Defense legislation and national industrial plans are government commitments about future resource allocation. When Congress mandates a new qualification pathway, it creates a services market. When it restricts covered-nation-manufactured equipment, it redirects procurement to a finite set of alternative suppliers. When a national government sets a production scale target and funds it through consecutive planning cycles, the signal is clear: policy-driven demand will shape domestic and export markets.

Congress enacted the FY2026 National Defense Authorization Act in December 2025. China released its 15th Five-Year Plan (2026–2030) in March 2026. Together, they represent the most significant simultaneous policy signals the additive manufacturing industry has seen. Each document stands on its own. When read and analyzed together, they describe a market structure that will look materially different in 3-5 years than it does today.

What the FY2026 NDAA says and what it signals

Six enacted provisions carry direct market structure implications for AM.

Section 832: The FAA bridge. DoD must now accept parts certifications issued by civil aviation authorities as valid military qualifications. Each military department must establish Expedited Qualification Panels with a 14-day decision window for alternate supplier approvals. This provision extends the Expedited Acceptance and Qualification process established in Section 865 of the FY2025 NDAA. Section 865 originally covered energetic materials, solid rocket motors, unmanned systems, space systems, and castings and forgings.

The signal for AM is direct. A decade of commercial aerospace AM qualification and certification work now has a statutory pathway into defense programs. That work was conducted under FAA oversight for aircraft structural and non-structural components. AM service bureaus and OEMs with existing FAA-certified parts portfolios do not need to restart the qualification and certification process for each defense application. The qualification asset they have already built has a new and larger addressable market.

Section 849: The covered-nation machine ban. Effective December 18, 2026, Section 849 prohibits DoD from operating or procuring AM systems from covered nations: China, Russia, Iran, or North Korea. The prohibition covers the machine, its operating software, and its network connectivity. A waiver mechanism exists but requires written certification to congressional defense committees, making routine use structurally difficult.

The market signal is straightforward. Section 849 closes DoD AM system acquisition to the global market's most price-competitive suppliers. The beneficiaries are domestic OEMs and allied-nation suppliers with established DoD relationships and compliant supply chains. Companies that have invested in cybersecurity architecture and DoD supply chain compliance are now structurally advantaged. This advantage applies to a market segment previously competed on price alone.

Section 871: AM in contested logistics. Section 871 includes advanced manufacturing in contested logistics demonstration requirements, establishing a statutory basis for forward-deployed and expeditionary advanced manufacturing capability development. This provision elevates advanced manufacturing from supply chain efficiency and ties it directly to rapid, distributed production of parts closer to the point of use. It opens a program development pathway that previously lacked explicit legislative backing.

Section 1841: The Civil Reserve Manufacturing Network. CRMN establishes a network of commercial manufacturers that DoD can rapidly activate to convert to DoD-directed production during periods of industrial stress. The provision covers advanced manufacturing explicitly. It requires DoD to develop a national registry of commercial AM capacity by process type and geography, with incentive structures for enrolled manufacturers. For AM service bureaus and contract manufacturers, enrollment in CRMN is both a revenue protection mechanism and a positioning tool.

Section 1842: The 24-month assessment mandate. Section 1842 requires product support managers to assess which critical readiness items can transition to advanced manufacturing within 24 months. The intent is to identify parts with supply chain vulnerabilities where advanced manufacturing represents a viable alternative source of supply. Those vulnerabilities include sole-source dependencies, excessive lead times, and unreasonable pricing.

This provision creates a structured demand signal. It requires DoD program offices to identify AM-producible parts and document the transition pathway, including expedited qualification process. For AM suppliers, this is a map of where DoD will be looking for solutions. For investors, it is a government-mandated assessment process. It will surface specific supply chain gaps and attach AM to the readiness conversation at the program level.

Section 1846: Cross-service qualification standardization. The Under Secretary of Defense for Acquisition and Sustainment and the Under Secretary of Defense for Research and Engineering now co-chair the Joint Additive Manufacturing Working Group. This elevates AM coordination to USD-level joint ownership. By September 30, 2026, the two Under Secretaries must review existing DoD qualification, acceptance, and supply chain policies and identify gaps specific to AM-produced products. By September 30, 2027, they must issue guidance covering process-based qualification (machine-by-machine, not part-by-part), data reciprocity to share test results across military departments, use of Section 865 expedited procedures, streamlined qualification for contractor-provided AM parts, incremental qualification that avoids full requalification when processes change, and a third-party certification option for entities that lack in-house expertise.

The market implications are substantial. The process-based qualification methodology is the statutory basis for what the industry has long called "qualify the process, not the part." The data reciprocity requirement provides the foundation for shared test results across services, meaning qualification work done for one program has a statutory pathway to inform another. The third-party certification option creates a new services market for accredited AM certification bodies. The September 2027 guidance deadline gives industry a defined window to engage the policy review process before positions harden.

China's 15th Five-Year Plan: what it says and what it signals for AM

The 15th Five-Year Plan (2026–2030), approved by the National People's Congress on March 12, 2026, does not name additive manufacturing explicitly. That absence is itself a signal worth noting. AM no longer requires its own named mandate because it has been absorbed into the structural categories that organize China's advanced manufacturing strategy. The relevant parent categories are 工业母机 (industrial mother machines), 先进材料 (advanced materials), 生物制造 (biomanufacturing), and 战略性新兴产业 (strategic emerging industries), all of which carry direct AM applications and all of which receive binding policy attention in this plan.

The plan's most consequential language for AM mandates "extraordinary measures" to achieve "decisive breakthroughs" across these categories. It adds a specific technical mandate for cross-scale manufacturing innovation (跨尺度制造等创新应用), which is the primary fabrication challenge in aerospace and defense structural components. It establishes a new industry standards pioneering program and calls for raising the level of standards internationalization. It further mandates the unification of military and civilian standards within the broader defense-civil industrial integration framework.

Taken together, these provisions create a policy environment oriented toward deployment and standardization rather than early-stage research. This is a meaningful shift in emphasis regardless of whether AM is named directly.

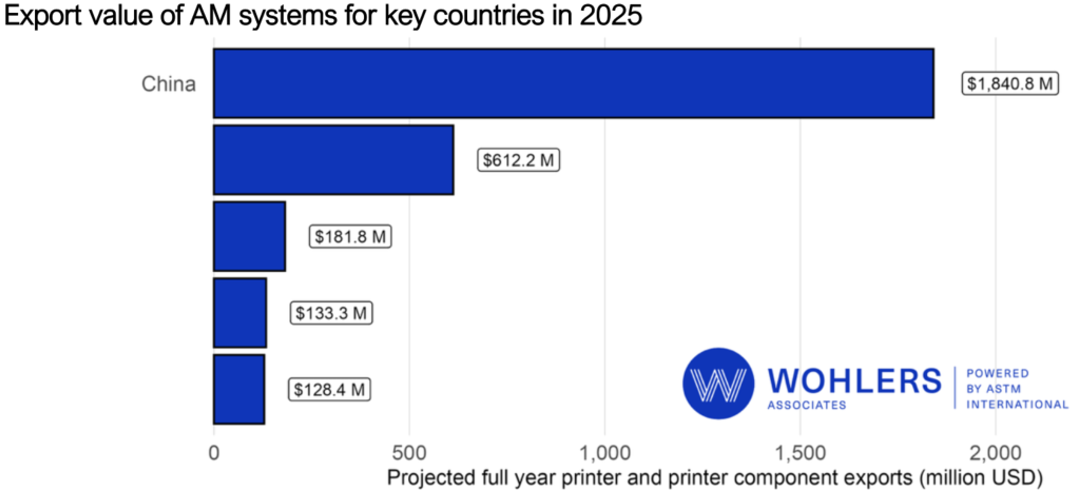

Understanding why China's AM industry has grown at the rate it has requires looking beneath the policy mandates to the mechanism that executes them. According to Wohlers Associates, China's AM industry reported 20–30% year-over-year revenue growth in 2024 and 2025. China's AM system exports reached $1.84 billion in 2025, approximately three times the nearest competitor.

Figure 1. Export value of additive manufacturing systems for key countries in 2025.

The conventional explanations such as low labor costs, government subsidies, and intellectual property–related factors cannot fully explain growth at this scale, however. Something else is doing the structural work. The investment framework known as the pyramid cultivation system (梯度培育体系) may be the primary driver behind such growth. This four-tier national SME development structure identifies manufacturers at the provincial level and scales the strongest into national Manufacturing Champions. Firms at each tier receive graduated state support: tax breaks, low-cost loans, procurement preferences, and access to government guidance funds. Tier status must be renewed competitively. Capital flows to firms that perform against defined metrics, not to firms that hold legacy relationships. These companies also benefit from placement in industrial clusters. Within those clusters, companies in the same technology areas share infrastructure and source required services. This structure reduces development costs and shortens iteration and adoption cycles. The result is a self-reinforcing industrial supply chain in which every supported firm strengthens the ecosystem around it.

Figure 2. China's pyramid cultivation system works akin to a sport league.1

A forthcoming article will examine the subordinate policy instruments that sit beneath the 15th Five-Year Plan. These documents name additive manufacturing explicitly and provide a more granular picture of how China intends to deploy the technology across priority sectors over the next five years.

What this means for the next 24 months

The FY2026 NDAA and China's 15th Five-Year Plan together describe a market that policy is restructuring from both directions simultaneously. DoD is closing covered-nation supply channels, creating new qualification pathways, mandating supply chain assessments, and building a commercial surge reserve. China is advancing industrial self-reliance, expanding AM exports, and developing its standards framework on an accelerating trajectory.

The companies and investors best positioned in this environment share one characteristic: they treat policy documents as forward intelligence, not compliance inputs. The provisions described above are not retrospective descriptions of what the market already looks like. They describe what the market will look like.

Wohlers Associates, powered by ASTM International, helps companies make the best possible strategic decisions in a rapidly shifting global landscape.

Footnotes

-

Brown, Alexander. "The accelerator state: Small firms join the fray of China's techno-industrial drive." Current History 123, no. Supplement 1 (2024): 40–49. ↩